COO @ Quorivex Systems

We wanted to automate a few workflows but weren't sure where to start. Lampros helped us cut through the noise and get something useful into production quickly.

CTO @ Teralynx Systems

They picked up our processes surprisingly fast and built around how we already worked instead of forcing us into a new system.

Financial Technology Company

We saw value pretty quickly. A lot of repetitive work that used to take hours every week simply stopped being a problem. Our team could focus on higher-value work instead.

Contact Us

Ready to Ship AI Systems to

Let's align architecture, execution, and delivery from day one.

Published On May 21, 2026

Updated On May 21, 2026

Every report your finance team produces manually is costing you more than you think.

Data pulled from multiple systems. Numbers cross-checked by hand. Formats rebuilt every cycle. And a review loop that eats days before anything reaches a stakeholder.

The cost of manual reporting in lending fintechs isn't just time, it's compounding.

Finance teams spend 75-80% of their time preparing data instead of analysing it.

Manual data entry in lending carries a 3.6% error rate, on numbers that investors, board members, and regulators are acting on.

85% of FP&A teams are already running beyond sustainable capacity.

The cost accumulates in places most CFOs never look. Here is exactly where, and what automated reporting for lending fintechs does about it.

Lets dive into it.

Ask any CFO at a lending fintech how monthly reporting gets done, and the answer is usually some version of: "We have a process."

What they mean is that someone on the team knows which system to log into first.

Here's what that process actually looks like:

Two to three days. One report type. Repeated every single month.

What makes this a genuine fintech reporting inefficiency, not just an inconvenience, is what sits behind those numbers.

Investors making portfolio decisions. Regulators assessing compliance standing. Board members are judging operational health.

All of them acting on data that passed through a manual process with no audit trail, no validation layer, and no way to confirm which version of the spreadsheet was actually the final one.

The process isn't incompetent. It accumulates quietly, through delayed decisions, reconciliation work, spreadsheet errors, reporting bottlenecks, and finance teams spending more time fixing data than analysing it.

And as lending operations scale, those costs scale with them.

The hours your analyst spends building reports are visible. What's harder to see and far more expensive is everything that happens around those hours.

Here's where the real cost is hiding:

How Manual Reporting Drains Finance Team Productivity in Lending Fintechs

Manual Reporting Errors in Lending: The Cost of Getting It Wrong

Compliance Risk of Manual Reporting for NBFCs and Lending Fintechs

Why Manual Reporting Fails to Scale With Your Loan Book

The Hidden Strategic Cost of Manual Reporting No CFO Is Measuring

None of these costs live on a single budget line. But together, they represent one of the most expensive operational decisions a lending fintech can keep making, the decision to do nothing.

Because once reporting complexity starts growing faster than the systems supporting it, finance teams stop operating strategically and start operating reactively.

That is the point where manual reporting stops being a workflow issue and becomes an infrastructure problem.

Automated reporting for lending fintechs is not about replacing your finance team.

It is about removing the part of their job that was never supposed to be their job in the first place, the manual assembly, the formula rebuilding, the copy-pasting, the chasing.

Here is what it actually looks like when it replaces the manual process:

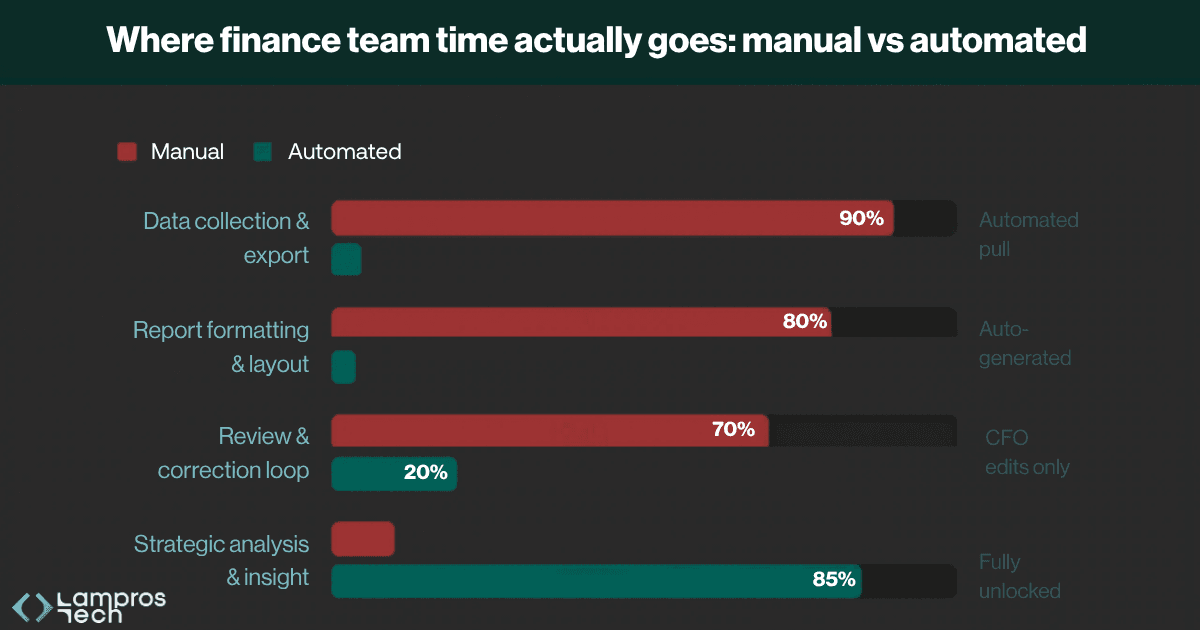

How Automated Data Collection Eliminates the Manual Pull

Instant Calculation, No Formula Rebuilding, No Version Drift

Auto-Formatted Reports, Right Format, Right Audience, Every Time

AI-Generated Commentary, Your CFO Reviews, Not Writes

Automated Distribution: Scheduled, Logged, Auditable

What changes for the lending fintech is not just speed. A report that took 2-3 days to produce manually is ready in minutes.

The finance team that spent 75-80% of their time on data preparation now spends that time on what they were actually hired to do: analysis, insight, and strategic input.

The CFO stops firefighting monthly reporting cycles and starts leading them.

The difference between manual and automated reporting in fintech isn't marginal.

It shows up in every dimension that a CFO, CEO, or CTO is measured on, speed, accuracy, compliance readiness, and the ability to scale without hiring your way out of the problem.

Here is what that difference looks like in practice:

Reporting Function | Manual Reporting | Automated Reporting |

|---|---|---|

Report build time | 2-3 days per report cycle | Minutes |

Data accuracy | 3.6% average error rate | 99.9% accuracy |

Audit trail | None, Excel and email threads | Full, every input, calculation and output logged with timestamp |

Regulatory readiness | Reactive, rebuilt each filing cycle | Always audit-ready |

CFO time on report prep | 75-80% of finance team time on data prep | CFO reviews finished draft, not builds from blank |

Scalability | Breaks under volume, needs proportional headcount | Scales with loan book at near-zero marginal cost |

Distribution | Manual sending, no delivery record | Scheduled, timestamped, logged automatically |

Compliance risk | High, no validation layer, no version control | Low, rules enforced consistently every run |

What This Means for Your Lending Operation

The numbers in that table are not aspirational.

They reflect what happens operationally when a manual reporting workflow is replaced with an automated one, and the gap between the two columns is not a technology upgrade, it is a different operating model entirely.

The Question This Table Is Really Asking

Every column in the manual side of that comparison is a cost your lending fintech is currently absorbing, in time, in exposure, in people, and in the decisions that never get made because your finance team is too busy producing reports to analyse them.

The question is not whether automated reporting for lending fintechs delivers better outcomes. The data makes that case clearly.

The question is how much longer the manual process runs before the cost becomes impossible to ignore.

This is exactly the workflow Lampros Tech is built to automate.

As an AI-native engineering partner, Lampros Tech deploys AI agents directly into your reporting stack, connecting to your loan management system, repayment tracker, and every other data source your finance team currently logs into manually.

From there, three things happen automatically:

The difference from other reporting tools is where the automation starts.

Lampros Tech does not polish the last step of a manual process, it replaces the manual process entirely, from data pull to finished report.

Manual reporting rarely feels expensive in the moment. It feels like routine work.

But across every reporting cycle, the cost compounds through analyst hours lost to reconciliation, spreadsheet errors reaching stakeholders, compliance exposure, and finance teams stuck maintaining reports instead of analysing the business.

The lending fintechs that scale efficiently are not the ones adding more reporting headcount. They are the ones building reporting infrastructure that runs automatically.

If your team is still pulling CSVs, rebuilding formulas, and managing report corrections over email every month, the cost is not future risk. It is already operational reality.

See how Lampros Tech automates reporting workflows end to end. Book a Demo.

The cost of manual reporting in lending fintechs goes beyond analyst hours. It includes time spent on data reconciliation, spreadsheet errors, delayed investor reporting, compliance risks, and the operational burden of maintaining reporting workflows manually every month. Many finance teams spend 75–80% of their reporting cycle preparing data instead of analysing portfolio performance and business risk.

Spreadsheet-based reporting creates risks around version control, manual calculation errors, weak audit trails, and inconsistent data validation. In lending fintechs, where investor reports, loan portfolio metrics, and regulatory filings depend on accurate reporting, even small spreadsheet mistakes can lead to compliance exposure, reporting delays, and incorrect financial decisions.

Most lending fintechs start by automating high-frequency and high-risk reporting workflows, including investor portfolio reports, loan book performance reports, repayment and delinquency tracking, board reporting, and NBFC compliance filings. These reports typically involve multiple systems, repeated manual reconciliation, and significant finance team effort.

Automated reporting improves finance operations by reducing manual data preparation, accelerating reporting cycles, improving reporting accuracy, and creating audit-ready workflows. Instead of spending days building reports manually, finance teams can focus on portfolio analysis, risk monitoring, forecasting, and strategic decision-making using real-time financial data.

Looking to Automate Reporting Across Your Lending Operations?

Replace manual spreadsheets, repetitive reconciliation, and delayed reporting cycles with AI-driven reporting automation built for lending fintech workflows.

Let’s Talk