COO @ Quorivex Systems

We wanted to automate a few workflows but weren't sure where to start. Lampros helped us cut through the noise and get something useful into production quickly.

CTO @ Teralynx Systems

They picked up our processes surprisingly fast and built around how we already worked instead of forcing us into a new system.

Financial Technology Company

We saw value pretty quickly. A lot of repetitive work that used to take hours every week simply stopped being a problem. Our team could focus on higher-value work instead.

Contact Us

Ready to Ship AI Systems to

Let's align architecture, execution, and delivery from day one.

Published On May 28, 2026

Updated On May 28, 2026

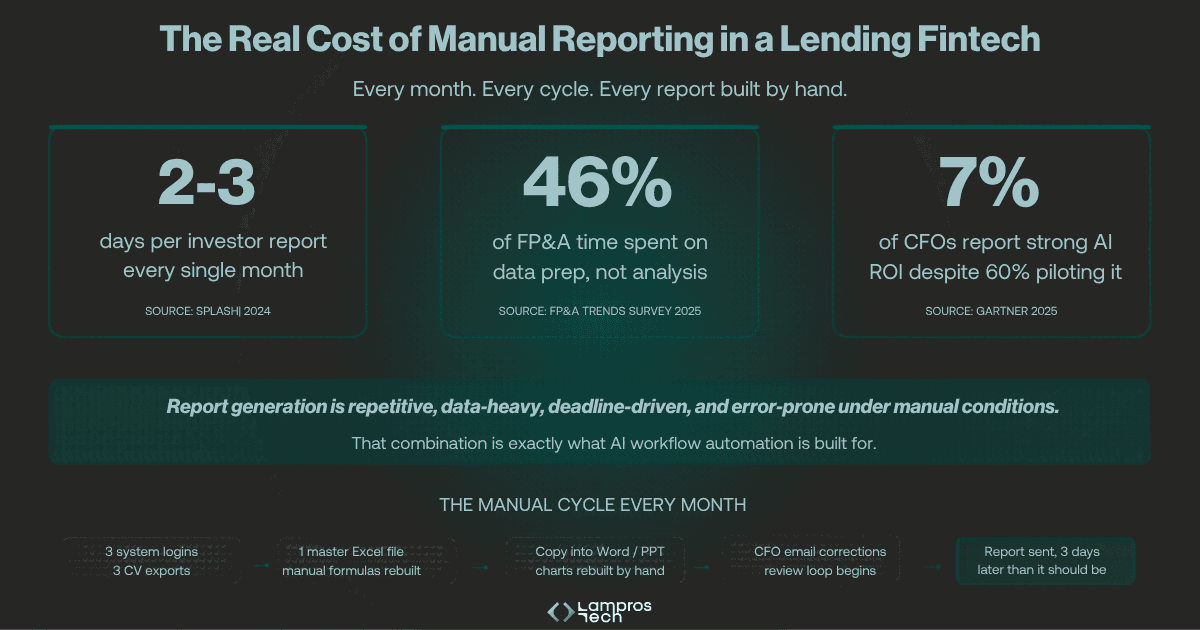

AI report generation for fintech is not a future capability; lending teams are already using it to replace a manual process that costs 2-3 days of finance effort every single reporting cycle.

Yet most lending fintechs are still running on three system logins, three CSV exports, one master Excel file, and a review loop that runs on email.

The cost is not just the hours. It is the errors sitting inside numbers that investors and regulators are treating as fact.

We have covered what this actually costs a lending fintech in Manual vs Automated Reporting in Lending Fintechs. This guide picks up where that one ends.

Report generation is repetitive, data-heavy, deadline-driven, and error-prone under manual conditions, exactly the combination that AI workflow automation is built for.

This guide covers how it works, what to evaluate, and how to implement it without disrupting current operations.

Understanding the boundaries before buying is what separates a successful implementation from one that automates the wrong thing.

AI report generation is the use of automated workflows and large language models to pull financial data from multiple sources, calculate key metrics, and produce a formatted, narrative-ready report, without manual intervention at any step.

For a lending fintech, that means the loan management system, repayment platform, and investor portal all feed into one automated pipeline.

The output is a finished report, correct format, correct data, AI-drafted commentary, ready for CFO review and approval.

It is not a dashboard. It is not a BI tool that surfaces charts for a human to interpret. One shows you data. The other produces a deliverable.

The distinction matters before you evaluate anything.

What It Does Not Do, Before You Evaluate Any Solution

Understanding these boundaries is the starting point for an implementation that actually holds up in production.

And the clearest place to start is with the reports already costing your finance team the most time every single month.

Not every report in a lending fintech is worth automating.

The ones that are share three characteristics: they run on a fixed schedule, they draw from the same data sources every cycle, and the cost of a manual error in them is high enough to matter to a stakeholder outside the finance team.

The 2025 FP&A Trends Survey found that 46% of FP&A time still goes to data collection and validation rather than analysis.

That is not a people problem, it is a workflow problem, and these three report types sit at the centre of it.

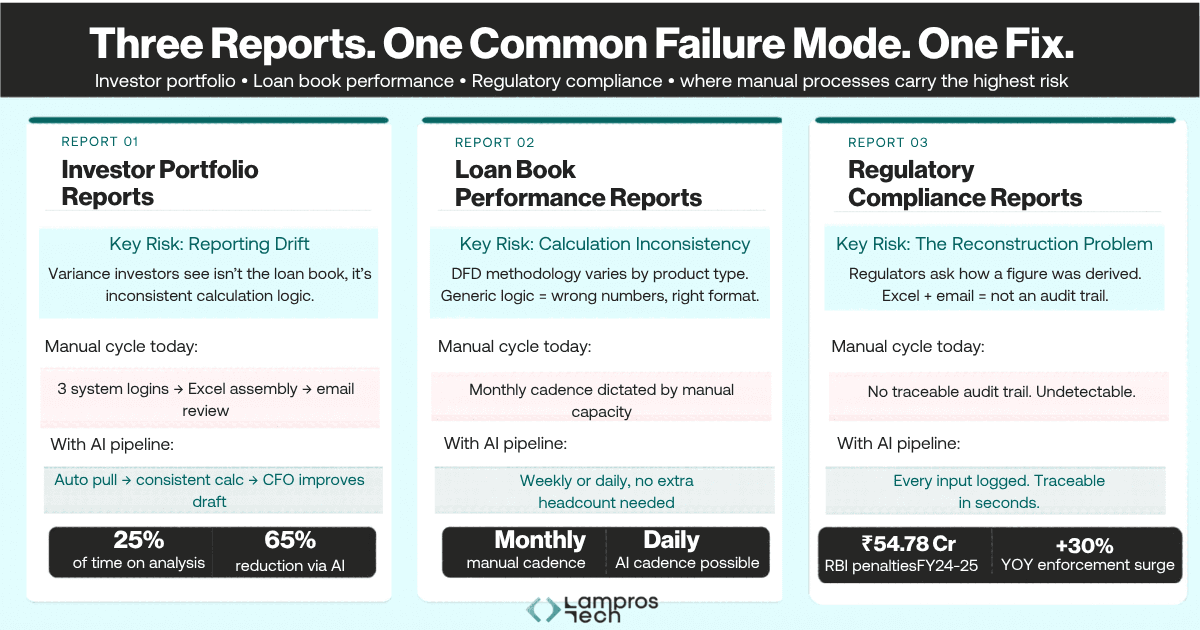

The specific risk here is not accuracy; it is consistency.

Investors comparing this month's portfolio report to last month's are looking for variance.

When two reports built by slightly different manual processes apply subtly different calculation logic, the variance they see is not portfolio movement.

It is reporting drift.

And reporting drift, even when the underlying loan book is healthy, raises questions in a funding conversation that are difficult to answer cleanly.

AFP and APQC research shows FP&A professionals spend only 25% of their time on value-added analysis, with the remaining three-quarters absorbed by data gathering and process administration.

Default rate methodology in lending is not standardised.

A fintech calculating days-past-due on a 30-day bucket this month and a 31-day bucket next month, because two different analysts built the report, produces a default rate variance that looks like portfolio deterioration when it is actually a measurement artefact.

That inconsistency creates material discrepancies in the data a Series C investor sees during due diligence, and those conversations rarely recover cleanly once a data integrity question has been raised.

RBI penalty data for FY 2024-25 shows ₹54.78 crore levied across 353 regulated entities, a 30% jump from the prior year, with reporting gaps and filing inaccuracies among the leading causes.

The reconstruction problem: When a regulator asks how a specific figure was derived, the honest answer in most manually-run fintechs is Excel formulas, email threads, and institutional memory.

A regulator who cannot follow the derivation treats that as a compliance gap, regardless of whether the number is correct. The report can be accurate and still be undefendable.

These three report types each depend on a reliable, repeatable data pipeline running underneath them, understanding how that pipeline works is what separates a successful implementation from one that inherits every problem of the manual process it replaced.

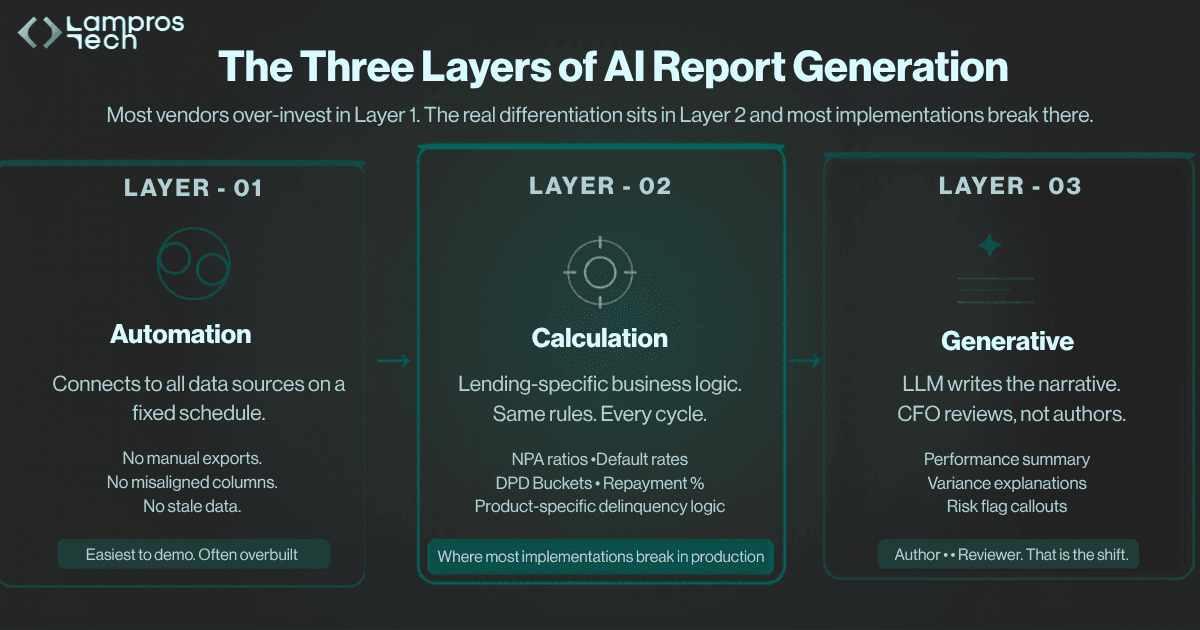

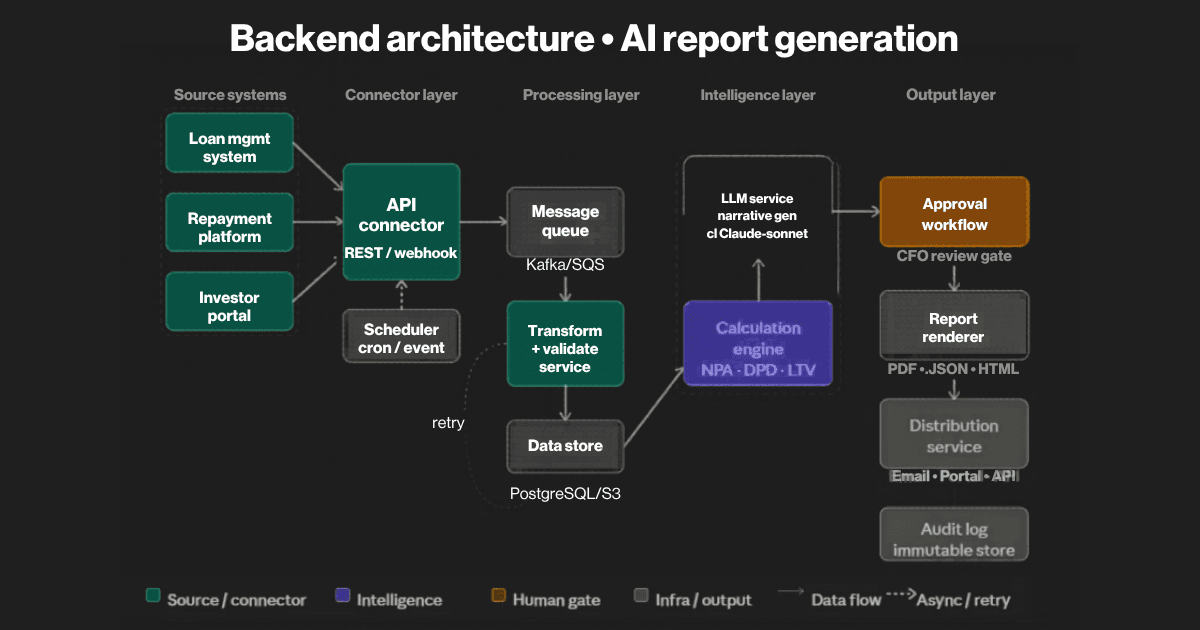

Most vendors describe AI report generation as a clean, linear process. In production, it is a distributed system with async message handling, domain-specific calculation logic, and a human approval gate that sits between intelligence and distribution.

A copilot helps your analyst build the report faster. An agent removes the analyst from the loop entirely.

For recurring, structured workflows, a copilot reduces manual effort by 30-40% while keeping the bottleneck intact. Agentic AI takes action, a copilot makes recommendations. For report generation, the action is the point.

Knowing the architecture is one thing. Knowing whether a vendor has actually built it, versus described it in a deck, requires a different kind of evaluation entirely.

Most AI reporting implementations that underdeliver were not let down by the technology.

They were let down by an evaluation process that never asked the right questions.

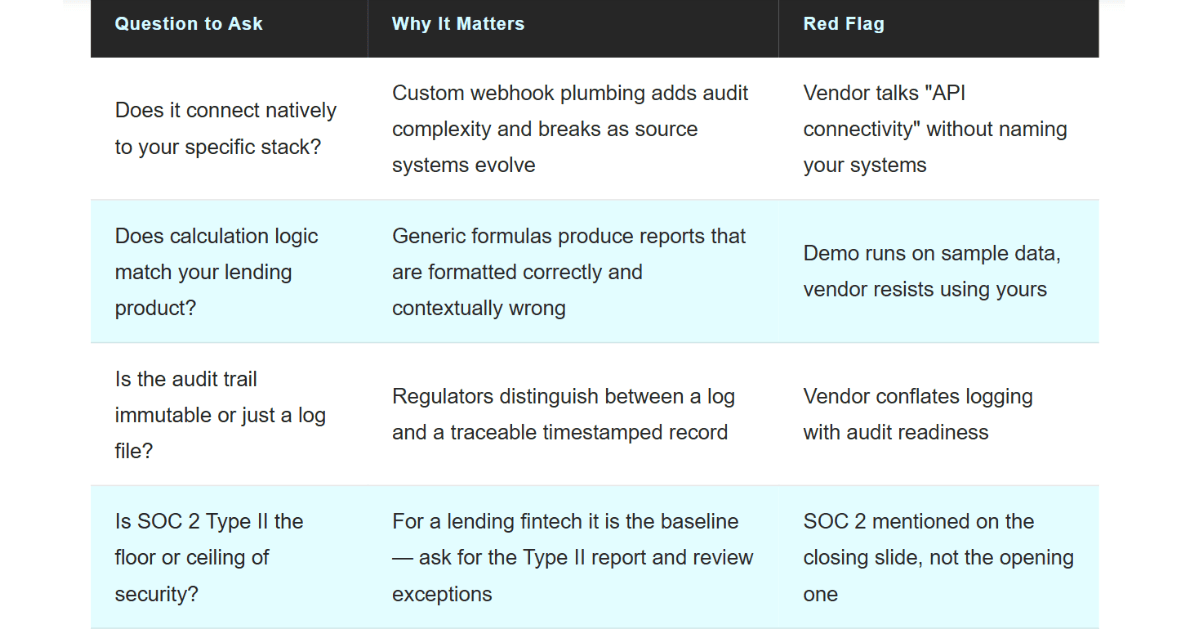

Before any demo, a lending fintech CFO needs clarity on four things:

These four questions will disqualify more vendors than any feature comparison will.

Knowing what to look for gets you to the right starting point. What it does not do is get the implementation right and that is where most fintech AI reporting projects lose the gains they evaluated for.

The irony of AI adoption in finance is well-documented; teams are too busy to implement the tools that would make them less busy.

The fix is not finding more time.

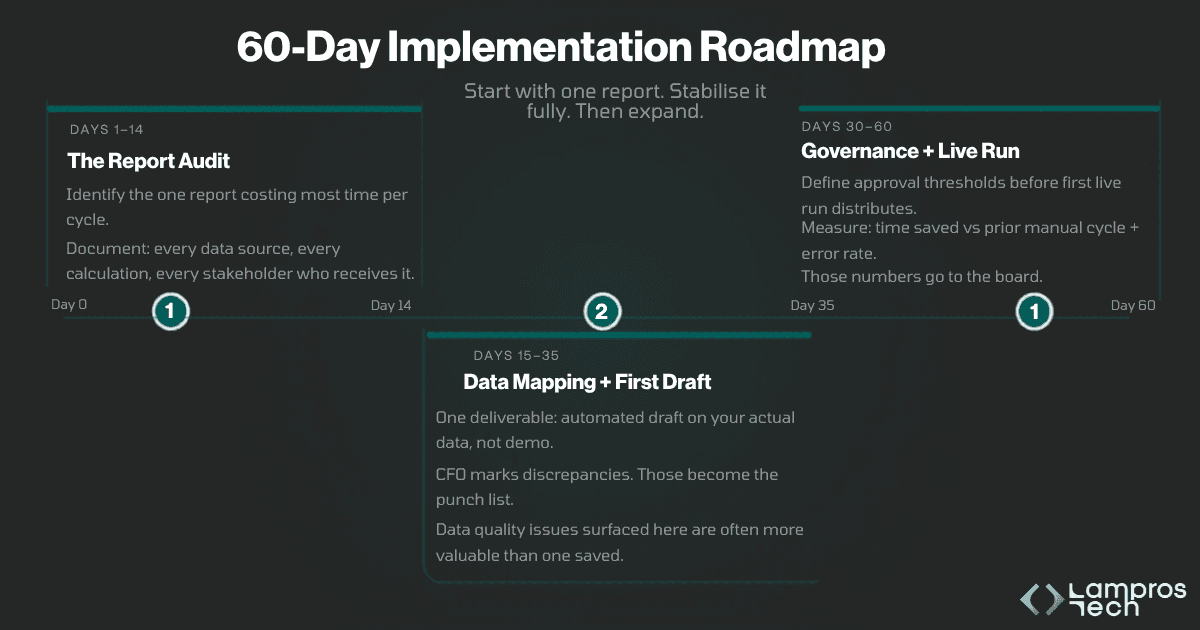

It is treating implementation as a core project with one non-negotiable rule: start with one report, not a transformation.

70% of AI implementations in finance had no measurable return in 2025, according to Softjourn's analysis.

The gap is not a technology problem.

It is a sequencing problem. The lending fintechs closing that gap are the ones that resisted the urge to transform everything at once.

A 60-day roadmap gets the first report live.

What it does not do is make every report worth automating, understanding which workflows AI handles well, and which ones it handles badly, determines whether the first implementation compounds into a sustainable function.

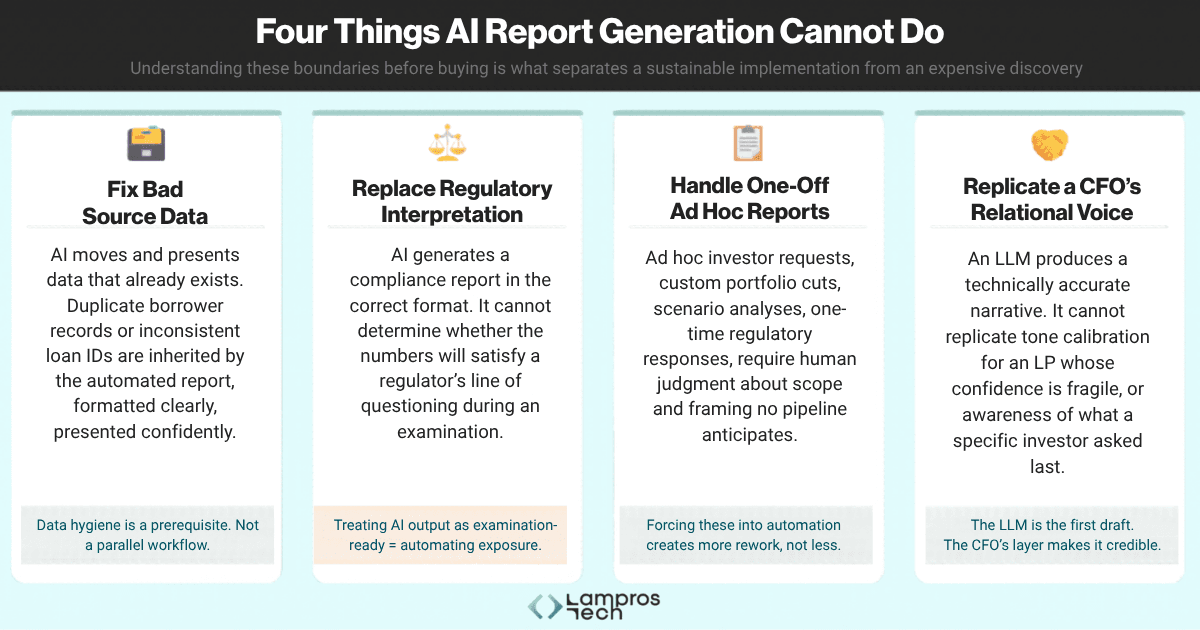

A CFO who deploys automation without understanding its boundaries will discover those boundaries at the worst possible moment.

These four limitations are predictable, avoidable, and worth understanding before implementation begins.

These limitations do not diminish the case for AI report generation they define the conditions under which it delivers.

Build the implementation around them rather than discovering them in production.

Manual reporting rarely feels expensive in the moment. It feels like routine work.

But across every reporting cycle, the cost compounds, through analyst hours lost to reconciliation, spreadsheet errors reaching stakeholders, compliance exposure, and finance teams stuck maintaining reports instead of analysing the business.

The lending fintechs that scale efficiently are not the ones adding more reporting headcount. They are the ones building reporting infrastructure that runs automatically.

If your team is still pulling CSVs, rebuilding formulas, and managing report corrections over email every month, the cost is not future risk. It is already operational reality.

See how Lampros Tech automates reporting workflows end to end. Book a Demo Now.

Yes, with a precise qualification. AI report generation is highly accurate for structured, recurring workflows where the calculation logic has been validated against your specific loan product type and the source data is clean. The accuracy question is not about the AI, it is about what you feed it. A well-configured pipeline running on clean, consistently structured data produces outputs that are investor-grade and regulatory-ready. A pipeline running on fragmented source data with inconsistent field definitions produces outputs that look accurate and are not. The distinction lives in implementation quality, not technology capability.

A BI tool surfaces data for a human to interpret and act on. AI report generation produces a finished deliverable, formatted, calculated, narratively written, and distribution-ready, with the human reviewing and approving rather than building. The practical difference: a BI dashboard still requires an analyst to spend 2–3 days assembling the investor report from the charts it displays. An AI reporting pipeline removes that assembly entirely. One shows you data. The other produces a document.

Not necessarily, but it requires someone who understands your source system APIs and can own the data connector configuration and validation rules during implementation. For most Series A/B lending fintechs, this sits with a senior engineer or a technical lead rather than a dedicated data engineering function. The practical constraint is not headcount, it is domain knowledge. The person configuring the calculation engine needs to understand your lending product's delinquency methodology, not just how to write a pipeline. That combination, fintech domain knowledge plus engineering capability, is what determines implementation quality, and it is worth asking explicitly which side of it your implementation partner brings.

The first measurable return appears in the first production run, time saved on the automated report versus the prior manual cycle. For a lending fintech where the investor portfolio report previously took 2–3 days to produce, that saving is visible immediately. The compounding return, error rate reduction, audit trail value, CFO time reallocation to strategic analysis accumulate over the subsequent three to six months as the pipeline stabilises and the finance team stops reverting to manual verification habits. Deloitte's Tech Trends 2026 report notes that leading organisations anchor AI initiatives to measurable business outcomes for AI report generation, those outcomes are time saved per cycle, error rate, and CFO hours reallocated to analysis. Measure all three from the first production run.

It can. Whether it should is a different question and the answer for most lending fintechs is no. Running three report types simultaneously in the first implementation multiplies the complexity, extends the validation timeline, and makes it impossible to isolate which report's logic caused the first production failure. The implementations that compound into a sustainable reporting function start with one report, stabilise it fully, measure the return, and use those numbers to justify the next phase. That sequencing is not caution, it is the discipline that separates the 5% of AI implementations that deliver measurable returns from the 95% that stall.

Ready to automate the report that is costing your team the most time right now?

Lampros Tech works with lending fintechs at Series A and B stage to build and implement AI reporting pipelines that hold up in production, starting with one report, not a full transformation.

Book a Discovery Call